Who Should Lead Digital Transformation in FSIs?

Smaller FSIs Have A Singular Advantage, But It Is Too Tedious To Focus On

Welcome to the second issue of the FSI Digital Transformation newsletter! Don’t forget to share it with your network if you find this newsletter is worth your time.

Who Should Lead Digital Transformation in FSIs?

When it comes to digital-related capabilities, a typical operating model of FSIs is the convolution of superficial re-orgs, political legacies, and band-aid roles. The mess is obvious to all stakeholders, but addressing it requires personal courage and knowing what good looks like. In the meantime, FSIs substitute “digital” for the names of traditional functions because it sounds cooler. The most pronounced example is of Chief Digital Officers (CDO). There are now thousands of them in the financial services and insurance industry, sometimes, even as a standalone role.

In 90+% of FSIs, “digital” usually means one of the two traditional functions, with large FSIs often employing multiple CDOs on the enterprise and LOB levels:

Customer/Partner Channels: AIG’s COO/CDO is “simplifying clients’ and distribution partners’ experience”, M&T Bank’s CDO is “providing customers with personalized experience"

Front-end Apps and Data: Pacific Life’s CIO/CDO is “unifying technology and data strategies”, U.S. Bank’s CDO is “making platforms to enable sales, onboarding, open banking”

A cooler-sounding “digital” title mostly adds to the organizational confusion by violating the cardinal rule of an effective operating model: clear delineation of everyone’s scope of responsibilities. “T-shape” employee profiles are only effective when the core responsibility is clearly defined and is separate from the colleagues. Is this particular FSI executive responsible for generating P&L from a specific market segment OR for enabling the generation of P&L by optimizing a specific supporting service?

Imagine, however, that FSI removes “digital” titles in its organization and use the actual area of responsibility instead. It would still leave us with a question: who should lead digital transformation (creation & acceleration of business value delivery)?

First of all, it should be a temporary executive who could drive successful change within a limited time while becoming increasingly redundant. Akin to an agile coach for a product team, the head of digital transformation is focused on the continuous leveling up of stakeholders with ongoing refinement of playbooks, only for significant use cases. While a strong Agile coach shall be out of a product team within 3-6 months, the digital transformation assignment is 2-3 years.

The background of a digital transformation executive must match the current phase of digital evolution in FSI:

Or in a simplistic version:

IT → Ops → Biz

Optimize tech → Automate business processes → Make money

If FSI is struggling with network outages or can’t get “waterfall” projects done on time, launching a fintech subsidiary or partnering with a no-code platform would be a guaranteed failure. Conversely, placing an IT executive who mastered the “IT Product” phase in charge of transforming a business model is also likely to fail. Generating significant P&L impact tends to require… P&L experience.

Here is how Mercury Insurance COO describes digital transformation expectations for CTO:

The CTO position represents Mercury's emphasis on the importance of technological innovation by building high-quality software and systems using modern development methodologies. The ability to rapidly assess, evaluate and deploy these solutions will allow the company to launch new products and services that will improve customer service, simplify agent processes, advance its data science and analytics capabilities, and position Mercury at the forefront of the industry's digital frontier.

Such hopefulness for “innovation” or “digital frontier” as transformation drivers are common among FSIs. Those FSIs spend years of effort and millions of dollars on “innovation” that is unlikely to have a material impact on their top line. Instead, once IT is optimized, FSI leadership should try switching from a top-down if-we-build-it-they-will-come mindset. Digital transformation must proceed bottom-up, in a specific LOB for a specific use case. And it should be led by a hands-on business executive who is willing to personally drive it, with enablement from IT.

Smaller FSIs Have A Singular Advantage, But It Is Too Tedious To Focus On

Smaller traditional FSIs are not designed to survive the 21st century. Today, a lack of scale means a suboptimal business model and an inferior value proposition to clients. Luckily for those FSIs, consumer apathy is the most potent force in the universe. Plus, top FSI incumbents are becoming increasingly opaque while leading startups - decreasingly focused. But those factors are just delaying the inevitable.

Cornerstone Advisors (Ron Shelvin via Forbes) illustrated the squeeze of small FSIs’ between big banks and fintechs:

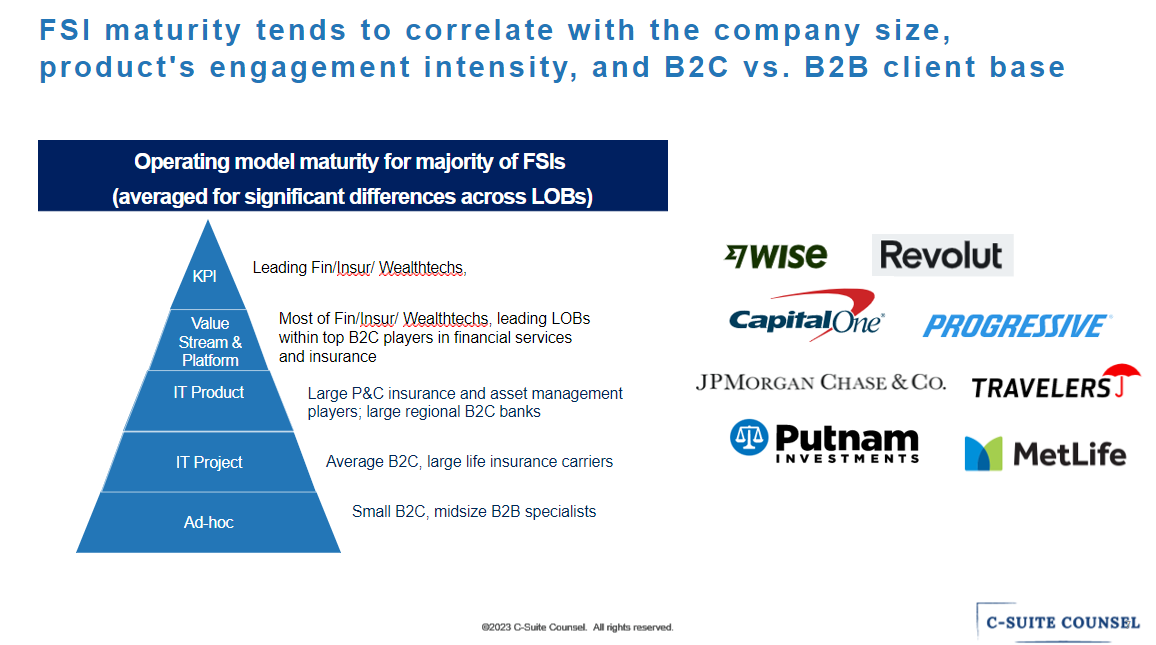

In the context of digital transformation, most of the smaller FSIs are 5-10 years behind top incumbents in digital maturity and even more behind leading fin/insur/wealhtech:

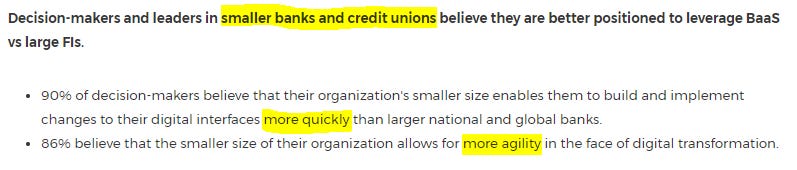

Yet, executives of smaller FSIs tend to delude themselves with the supposed advantage of their size, namely agility (source: NovoPayment & Forrester):

So why haven’t small FSIs transformed faster yet? Similar to larger FSIs, both tend to chase the same set of cool technologies (AI, Cloud, API) and products (BNPL, Robo, Telematics). Except, smaller FSIs don’t have sufficient talent quantity and the budget to scale all of them concurrently. Even if a smaller FSI makes faster strategic decisions (many don’t), focusing on just one or two launches at a time is the only road to success.

Where to focus its limited capabilities is also a simpler question for small traditional FSIs. Its only differentiation is the intimate knowledge of the local customer. While dominating incumbents and startups are attempting mass personalization, they are not yet capable of consistent micro-targeting. Smaller FSIs are in a better position to identify and prioritize the most crucial pain points and then create a lasting differentiation, one customer segment, and one feature at a time.

Sounds simple enough, but in my experience, less than 20% of smaller FSIs’ executives are able to stay focused on one-two use cases and be excited to learn directly from their customers. They find it uncomfortable, risky, boring, or simply not a part of their jobs. Focus and field engagement is tedious, but it’s the only way for a small FSI to survive and maybe even flourish. Embrace the grit.

Great start with these first two pieces Yakov. I’m passing this on to others I work with.