Would Recession Be a Wake-Up Call for Unconstrained Digital Transformation in FSI?

Also in this issue: What Is and What Is Not Digital Transformation in FSI?

Would Recession Be a Wake-Up Call for Unconstrained Digital Transformation in FSI?

As Western society enjoys the Age of Decadence, so do FSIs, who have collectively invested billions of dollars in digital innovation labs/garages/accelerators, hired dedicated Chief Transformation or Innovation Officers, and formed Agile groups. While there may have been some justification for this spending, including hopes that a blockchain or an AI pilot or a fintech partnership would be the "silver bullet" to generate significant profits, much of the innovation and digital transformation has been driven by opulence rather than rigorous financial analysis.

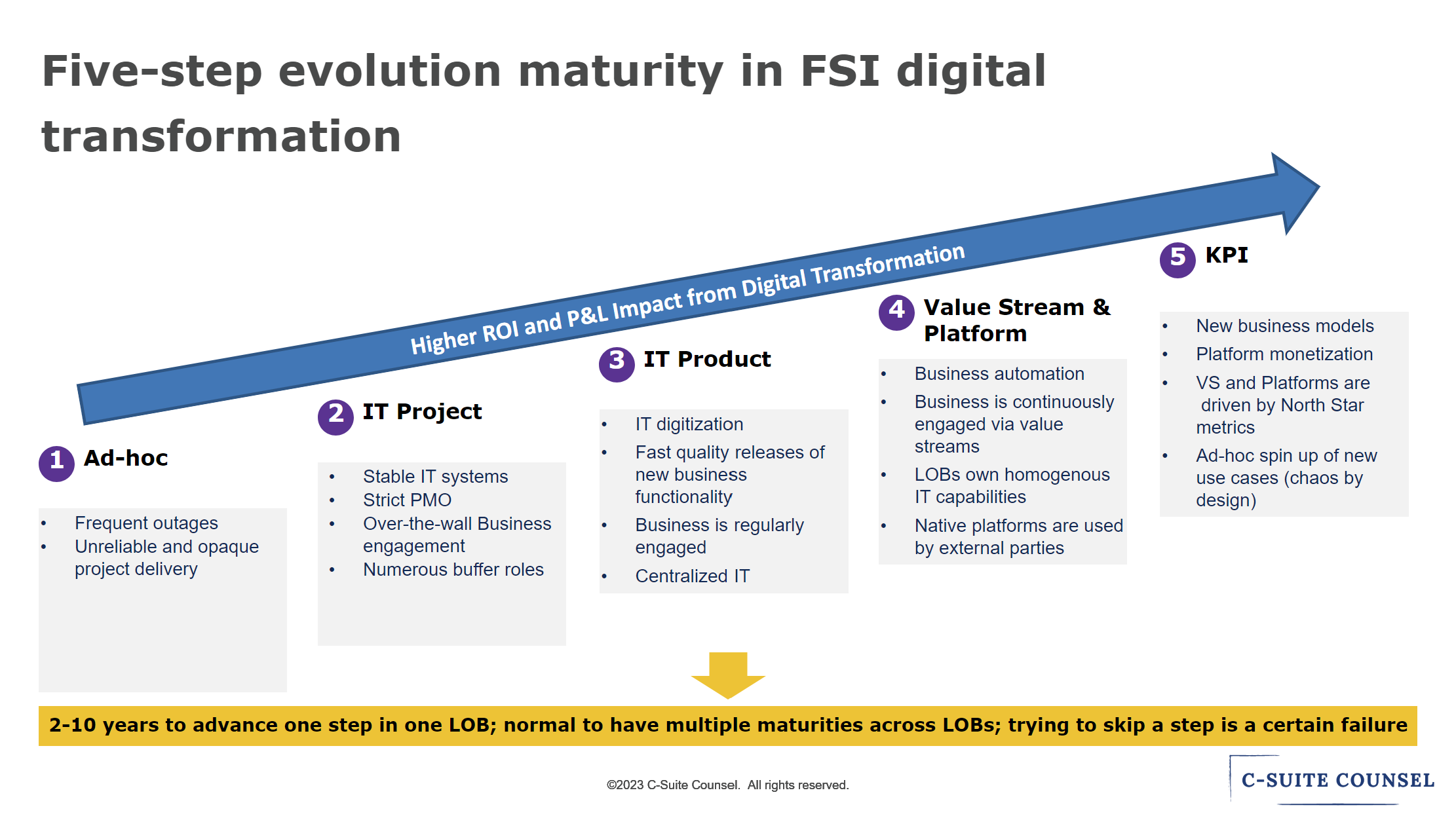

The tangible positive aspect of digital transformation in FSI is that each year more and more companies are approaching the completion of the foundational phase and achieving IT Product maturity. Certain FSI LOBs have even reached a level of comfort in scaling value streams and platforms. Regardless of the FSI segment and even with ineffective investment, the rising tide of spending 5-10% of the revenue on digital transformation is sufficient to elevate the majority of companies. However, as the global FSI industry spends $1 trillion annually on digital transformation, it is becoming increasingly challenging to justify such expenditure due to the diminishing list of remaining use cases that could create a transformative impact.

Let's explore the most promising digital capability of the 21st century, ChatGPT. The unique and thrilling qualities powered by generative AI have garnered significant attention. In fact, Mistral AI managed to secure €105m in funding without even having a prototype. Instead, they simply produced a 7-page write-up that emphasized an open AI model with a founding team consisting mostly of individuals with AI backgrounds. Voilà.

We briefly touched upon ChatGPT in our first newsletter, and since then, there has been more clarity regarding its potential use cases. Would ChatGPT end-up creating transformative or marginal value? Consider the slide below:

To simplify, a customer sub-segment that prefers a chat interaction would get even better bot support. What is the likelihood of this significantly reducing customer attrition or manual call center efforts? It is not high. Consider this ChatGPT pilot of Ally Bank:

Ordinarily after a customer service representative finishes assisting someone they input notes about the call. In the pilot, ChatGPT is inputting the notes. The objective is to see if this will free up time for the representatives to handle more calls.

Maybe it would free up some call center employee capacity and it could be a good opportunity ROI-wise, but it wouldn’t lead to a transformational impact of eliminating a sizable portion of the service calls or call center staff.

Similarly to AI, there is an increasing evidence that cloud technology doesn't generate a transformative impact. The migration to the cloud could benefit some FSIs that want to reduce complexity or don't have in-house cloud expertise, but it's unlikely to save a lot of money. With so many end-user features already deployed by FSIs without much adoption, is the promise of increased velocity from leveraging the cloud likely to generate a significant P&L impact? It is unlikely as FSIs seem to be approaching the point of marginal returns with CX. According to the recent Forrester study, “since the pandemic, the average CX quality for multichannel banks in the United States has dropped and the average CX quality for U.S. direct banks has flatlined.”

Even if digital transformation does not offer many untapped value generation opportunities, could it play a critical role in protecting FSI incumbents against digital native startups? Answer: there is no need. The decade-long rumors of imminent FSI disruption have been greatly exaggerated. Consider this real-life example of a home insurance quote that compares incumbents against two of the more prominent insurtechs in the US, Lemonade and Hippo.

You wouldn't choose either of those insurtechs. Hippo doesn't offer sufficient insured value, while Lemonade has inferior product pricing for similar features when compared to Progressive and Liberty Mutual. Not surprisingly, the stock prices of both Lemonade and Hippo are down 90-95% from their highs.

Without a significant upside in value creation or the imminent threat of disruption, the case for digital transformation becomes quite challenging. Currently, Wall Street analysts may get excited by flashy announcements of massive FSI spending on AI, API, and Cloud. However, even they will eventually become more discerning and start asking ROI-related questions. This shift in mindset typically occurs towards the end of business cycles, also known as a recession, which the world economy seems to be facing sometime by 2025.

After a decade of top-down innovation in FSIs, fueled by opulence and the pursuit of a 'silver bullet,' will it finally transition into bottom-up creativity, as advocated by Ron Shelvin (refer to “The End of Innovation” link at the bottom)? Alternatively, if the Western economy manages to avoid a severe downturn, will the unconstrained digital transformation continue unabated? If history serves as a guide, FSIs are likely to experience a significant slowdown in digital transformation spending, prompting them to learn how to prioritize impactful use cases more effectively. However, a few years later, the cycle of innovation bureaucracy will likely resurface, bringing back the fun times once again.

What Is and What Is Not Digital Transformation in FSI?

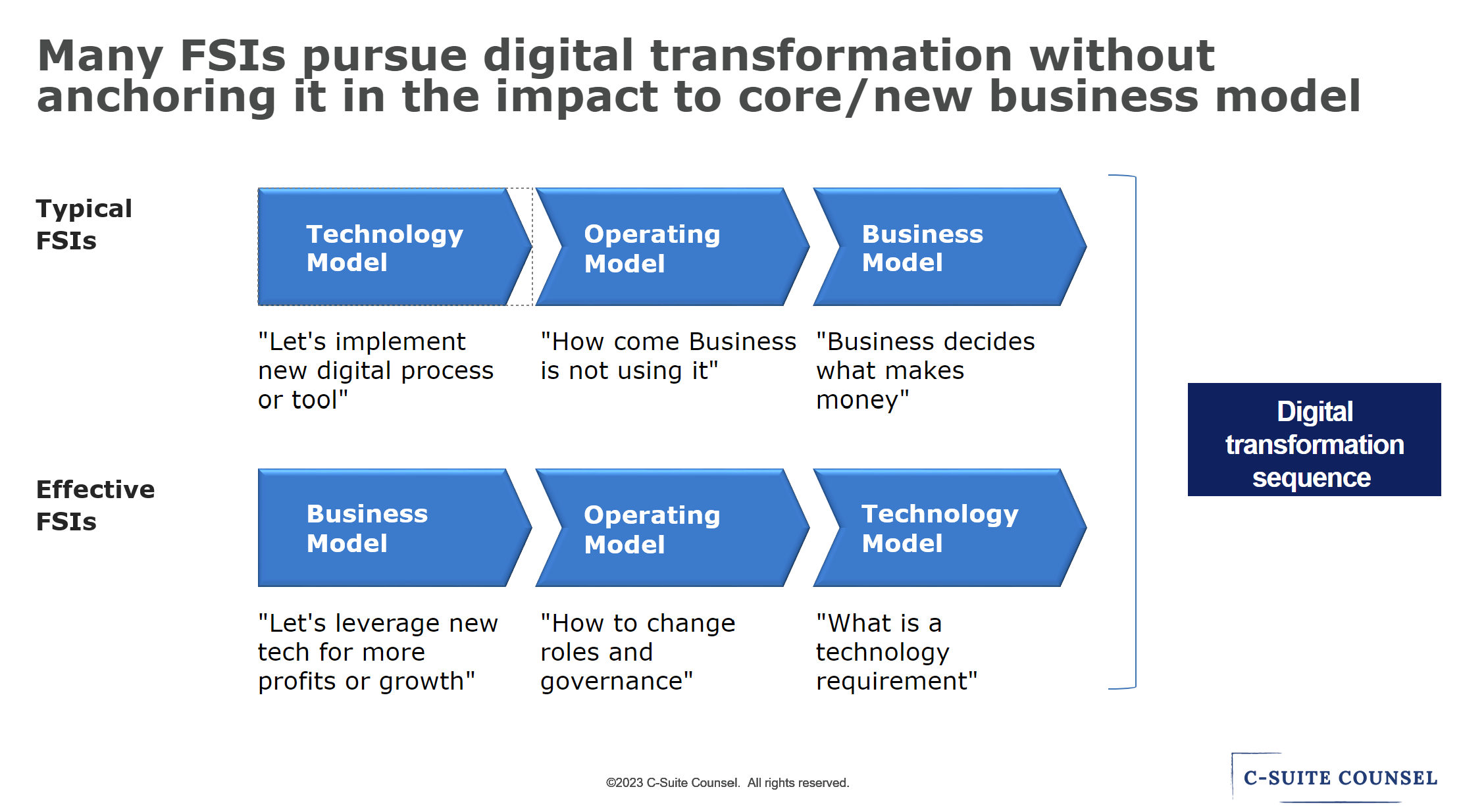

As we discussed in another newsletter, digital transformation in FSI has reached its peak of hype. Companies are now allocating 5-10% of their annual revenue to these initiatives, and investors often base their recommendations on the magnitude of spending rather than a deep understanding of the eventual ROI. Consequently, the digital transformation spend bucket has become a mix of both genuinely transformative initiatives and standard IT-related projects. Let’s now distinguish between mere the acts of wishful thinking or phantom transformation and the true transformation in FSI.

1. Business model

The ultimate purpose of digital transformation in FSI is to bring about a significant improvement in the business model. Otherwise, digital transformation can be excessively costly and risky. If you hold a different perspective, I encourage you to read this newsletter for supporting evidence and share your thoughts in a comment.

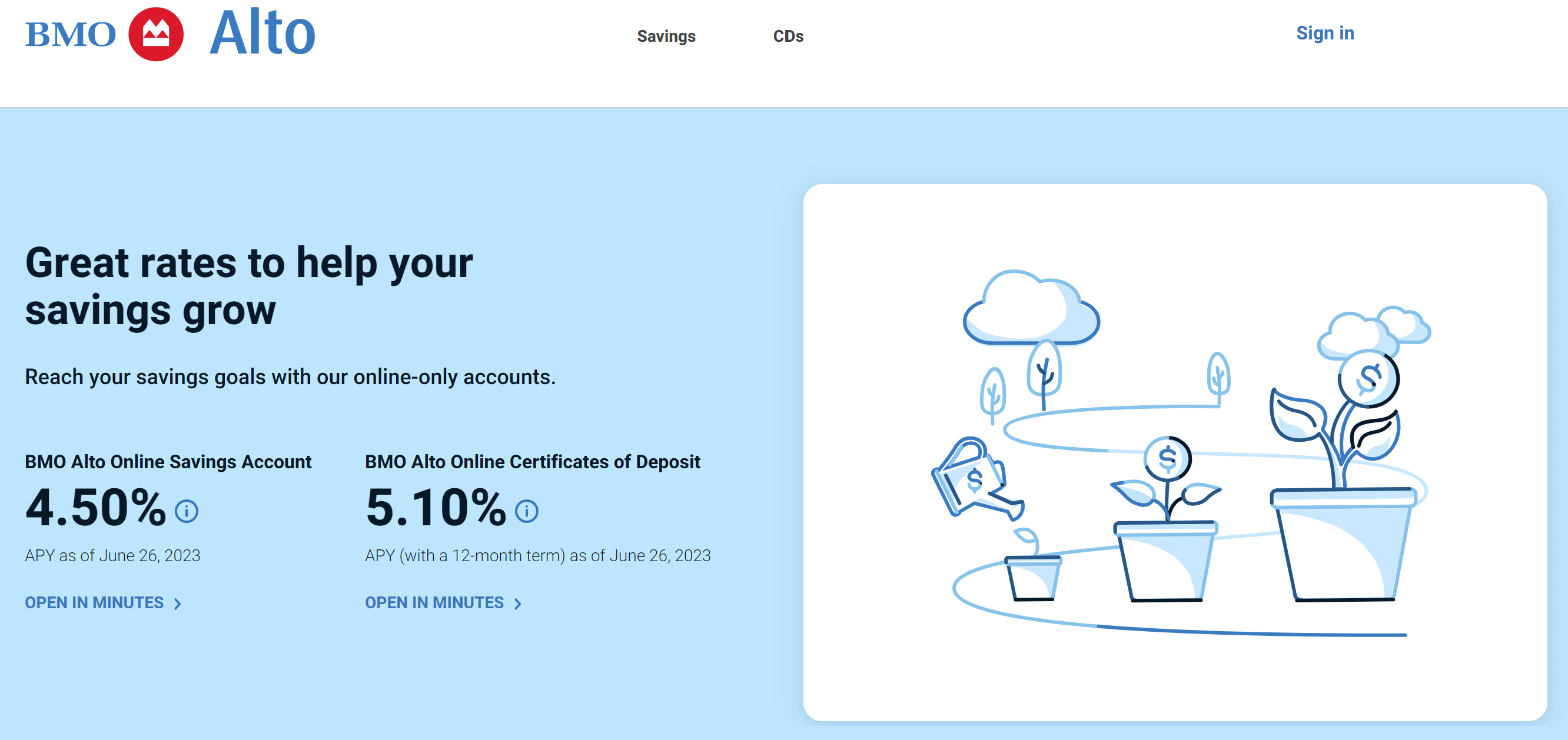

a) Digital transformation example: BMO launching a digital-only subsidiary in the US with separate P&L and distinct product pricing, BMO Alto.

b) Traditional initiative example: State Employees’ Credit Union rolling out e-signature pads to branch employees.

SECU team members will use these devices to help members expedite the signing of loan documents. Additionally, our financial advisory services specialists are piloting the use of iPads to deposit member checks when members open an investment account or want to invest additional funds.

2. Operating model

The success of achieving a new business model relies on the operating model. If the business model represents the "what," then the operating model represents the "how." True digital transformation entails leveling up the operating muscles of FSI employees, beginning with the executives. Consequently, this process tends to occur gradually and often faces resistance at all ranks.

a) Digital transformation example: TD Personal Bank Canada pursuing an autonomous cross-functional team structure that requires back-office groups to enable business lines rather than pursue function-centric initiatives.

b) Traditional initiative example: establishing a permanent Agile function to act as a buffer among siloed groups that are hesitant to level up their operating muscles.

3. Technology model

A technology model change often becomes a favored solution for FSIs seeking to easily reap the benefits of digital transformation without undertaking the challenging task of transforming their business and operating models. Consequently, many FSIs have made excessive investments in advanced technology capabilities without effectively connecting them to the required upstream changes. This leads to a surplus of unused technology and data capacity, leaving CIOs wondering why the business does not seek their guidance on leveraging these resources.

a) Digital transformation example: MassMutual connecting API, AI, and data.

“In the early days of getting all of this work started, it was just the basics… We set up a data governance team, got the right tooling and process in place… Fast forward to today. We invested a lot to provide easy-to-use abstractions on top of all that data. When we build our micro services, we use an enterprise object model, a common logical way to represent all the data in the company. We make that data available to our developers so they have just one way to think about and consume all that information…”

b) Traditional initiative example: Delta Community Credit Union deploying a business glossary that helps organizations manage and classify data more efficiently.

The software enables DCCU to tag and categorize data, show what rules were applied during data transformations, and help business users serve themselves… With OvalEdge, business users can now understand how data sources were built, where data is coming from and what rules were used to create metrics.

Schwarzberg | Inside WEEL | Medium")

The next time you encounter someone referring to a traditional initiative as "digital transformation," don't hesitate to challenge them. By doing so, you can ensure that the necessary effort aligns with the expected impact and better prepare your organization for genuine transformation when the need arises.