Are There Any Boring FSI Segments, or Just Unambitious Executives?

Also in this issue - FSI Executives Confront Choice: Meetings or Digital Transformation?

Are There Any Boring FSI Segments, or Just Unambitious Executives?

When traditional FSI executives observe the remarkable achievements of fintech disruptors such as Stripe, Wise, Ramp, and Revolut, how can they justify their failure to replicate similar successes in their own organizations? Traditional FSIs possess greater industry knowledge, more resources, particularly in the initial stages, and stronger relationships with regulatory bodies. They deployed digital channels a long time ago and had access to the same vendors as those fintechs when they were launched. Furthermore, they were aware of the singular best practices from Amazon, Netflix, and Spotify that every successful fintech follows.

One logical explanation could be that we're witnessing the fortunate outcomes of a thousand massive gambles. A successful fintech might easily require a billion dollars of investment even before its IPO. Unlike venture capitalists, who have access to half of a trillion dollars in "dry powder" alone, no FSI can feasibly undertake such a multitude of high-stakes endeavors. Consequently, a traditional FSI is constrained to place only a handful of bets, which, given the exceedingly infrequent and unpredictable nature of breakout successes, often proves insufficient.

1. Concentrated bets

However, traditional FSIs regularly make substantial bets. And this isn't even considering the staggering $1 trillion that traditional FSIs allocate annually for technology expenditures. Nor is it addressing the billions they squander on fintech subsidiaries in their endeavors to leapfrog digital transformation. No, FSIs consistently place significant bets within their core business offerings, determining which ones receive optimal digital resources and which ones are left with scraps. As a result, a noticeable chasm in digital maturity often exists among different lines of business within the same financial services and insurance organizations. For instance, Capital One might prioritize Credit Cards, Progressive might emphasize Auto Insurance, Fidelity might concentrate on Personal Investments, and so forth.

Those bets are clearly concentrated and collectively surpass the funding of fintechs within the same niche. Similar to fintechs, FSIs identify open spaces and customer pain points to direct their resources. The primary distinction lies in how the traditional FSIs approach innovation. In contrast to startups, which often depend on disruptive business models and aggressive marketing, leading FSIs seek out points of leverage within their existing capabilities: client data, product expertise, internally developed platforms, and the like.

The reason why fintechs find success in certain areas while facing challenges in others is primarily linked to the transformation pace maintained by some FSIs. This dynamic plays a pivotal role in minimizing the likelihood of disruption. The limited success of disruptors in fields like consumer credit cards, auto insurance, or personal investments can be attributed to leading FSIs within those niches effectively addressing significant pain points.

Therefore, a more thought-provoking inquiry pertains to why specific traditional FSIs fare better than others in their competition against a multitude of disruptors.

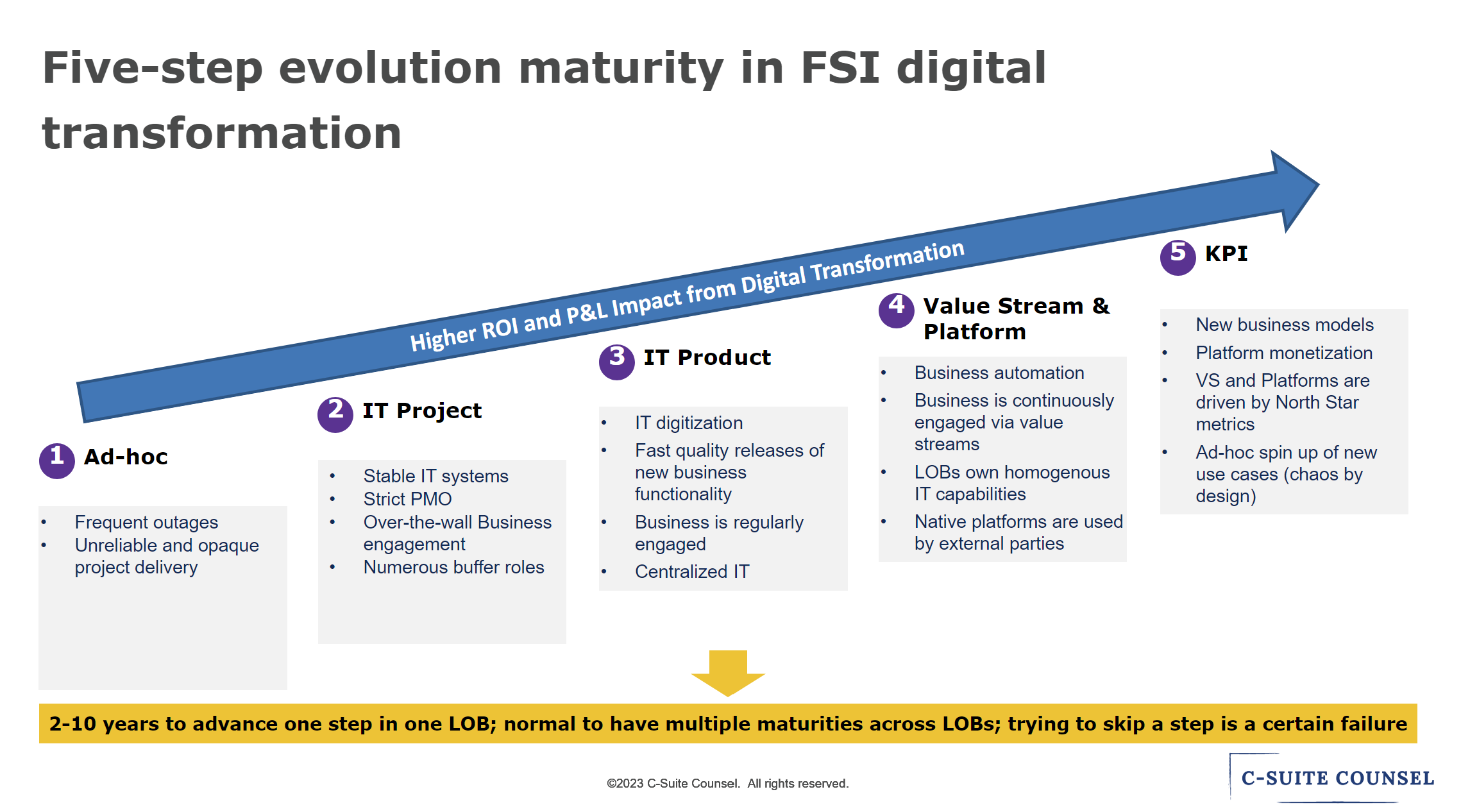

The answer is straightforward: the narrower the gap in digital maturity between a leading disruptor and prominent traditional FSIs, the less probable the disruption becomes. To illustrate, in the U.S. auto insurance sector Progressive stands not just on par but ahead of insurtech companies like Root, Lemonade, and Hippo in various crucial digital competencies. Each entity operates at approximately Level 4 of digital maturity. In the realm of cross-border money transfers, Wise (and to a lesser extent, Remitly) possesses a considerable lead over Western Union in digital capabilities, a Level 5 digital maturity versus Western Union's Level 3.

Some traditional FSIs are so exceptionally advanced in their digital maturity that they even attempt to monetize internal platforms. This endeavor is exceedingly challenging, as it demands competitors to pay for services. BlackRock's Aladdin stands as one of the rare success stories in this regard.

2. Less disruption less problems

On the opposite side of the spectrum, numerous FSIs need not fret about disruption. Capitalism abides by two rules: "Give customers what they want" and "Don’t get high on your own supply." Any FSI that violates these principles by introducing unwanted digital products or overspending on internal digital capabilities typically faces adverse consequences. However, the majority of FSIs exercise prudence by aligning digital investments with customer preferences. They rarely invest heavily in areas where customers aren't clamoring for enhanced digital functionalities, and they avoid digitizing Finance at the detriment of Sales.

The same principle largely applies to digital transformation in FSIs. We frequently emphasize that digital transformation should be primarily motivated by its impact on the company's P&L. Eventually, an FSI's leadership develops a hypothesis that they are lacking a valuable digital capability for which customers would be willing to pay a substantial amount. Following attempts to address this opportunity through vendors and consultants, the FSI often realizes that a complete transformation of its business and operating models is necessary. It's common for the FSI to discover that its current digital maturity is quite basic, necessitating a delay in monetization until the organization achieves a more advanced level of maturity. Over time, however, the FSI can gradually unlock substantial revenue potential from these enhanced digital capabilities.

Given that clients' willingness to pay for new digital capabilities is the pivotal criterion, digital transformation's progress varies across different FSI products and customer segments. B2B transformation usually lags behind B2C, and within FSI, areas like insurance tend to trail payments in terms of digital adoption.

The same principle applies to fintech funding as well. VCs prioritize investments in FSI segments where there is greater client demand (alongside less digitally mature incumbents, as discussed in the previous chapter).

3. Who said title insurance is boring?

This general pattern has one notable exception: the monetization of data. Situations arise where an FSI's primary customers might not be inclined to pay significantly more for new digital capabilities. However, the FSI may possess data of considerable value, attracting interest not from clients or competitors but from an entirely different array of companies. In such instances, the FSI need not necessarily transform its core business, as long as it can enhance its proficiency in scaling and marketing data platforms.

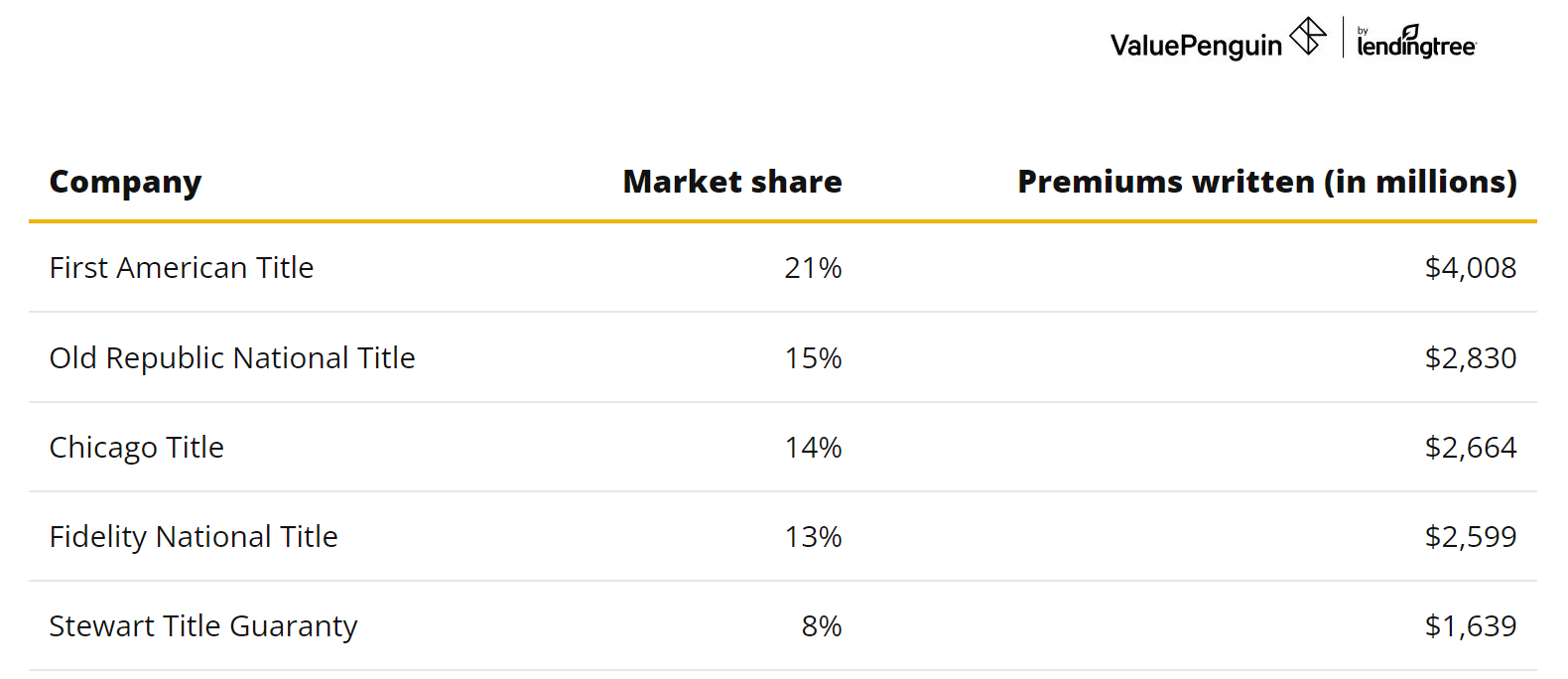

When I initially encountered the title insurance industry several years ago, their technological capabilities were as one might anticipate - notably lagging behind the majority of other FSI segments. Simply examining the names of the top five players in the US, they appeared entrenched in old-fashioned and traditional practices:

Later, I stumbled upon an intriguing revelation: certain companies within this industry harbored data businesses that outpaced their parent organizations in terms of advancement. Take First American, for instance, which remarkably dubs itself 'the leader in the digital transformation of its industry.' This claim holds true as the company excelled in data monetization as a distinct venture. Rather than transforming the core business, which might be too mundane for advanced digital features, First American focuses on the area that could generate a substantial return.

So, when an FSI isn't undergoing digital transformation, it's worthwhile to double-check if it truly occupies a hidden niche devoid of substantial disruption risk and monetization potential. Alternatively, its executives could explore newfound ambitions, drawing inspiration from the title insurance industry's innovative approach.

FSI Executives Confront Choice: Meetings or Digital Transformation?

FSI Executives adore meetings. They might deny it, or even gripe about them, yet meetings reign as the favored activity in their professional realms. They arrange these gatherings, fully aware that a vast majority of employees (92%) deem them unproductive, and a significant portion (43%) could be axed without consequence. But that's not all. If a more senior figure cancels a series of meetings, the majority of executives would insist on its revival, all while initiating an entirely new series of meetings to preserve the delicate equilibrium between these sessions and less interesting tasks.

Simultaneously, meetings stand in opposition to digital transformation. The most proficient FSIs and fintechs adopt an anti-meeting ethos, channeling all available time towards action and contemplation. Digital transformation propels autonomy to the forefront, empowering frontline employees and reducing the domain of middle-management bureaucracy where meetings often thrive. Scaling, by its very nature, involves expanding the enterprise while shedding the weight of meetings, which at best provide little value and at worst impede progress.

Shopify conducted a data-driven experiment. In January 2023, the company eliminated one-third of the meetings from employees' calendars, leading to an increase of over 15% in completed projects and enhanced business fundamentals.

So, why do FSI executives persist in their fondness for meetings despite evidence to the contrary? And what alternative actions should they take instead?

1. Creating the right perception

"What are you talking about? It was a highly successful initiative!" shouted an executive from a top-10 insurance firm in front of the C-Suite during my presentation. The company squandered tens of millions of dollars on two gold-plated data centers. The project was well beyond the budget and timeline, and the data centers themselves remained only half occupied. Throughout interviews, I repeatedly encountered this debacle cited as an example of the company's preference for ill-fated top-down initiatives over more agile bottom-up efforts. Interestingly, not long after, the company made the decision to transition to cloud infrastructure. Nevertheless, my assertion that the initiative had fallen short of expectations was met with resistance from its champion, who was aspiring to promotion.

A typical FSI executive expends an exorbitant amount of effort to meticulously craft a favorable perception of themselves among the decision-makers. This is a result of functioning within a bureaucratic framework where performance metrics are often malleable and qualitative. Consequently, in this context, the ramifications of displeasing influential individuals far outweigh the potential risks of strategic initiatives falling short. In this environment, the adage "perception is reality" holds true, leading these FSI executives to use meetings as a means to garner support from key figures, not necessarily for strategy or solutions (as those are usually dictated from the top), but for shaping how they are perceived.

2. Complaining about others

As previously discussed in a different newsletter, FSI executives often display a penchant for complaining. Rare is a discussion where I don't hear their grievances about their company, peers, bosses, or employees not meeting their standards. This inclination stems from a fundamental human protective mechanism. When our personal or professional involvements fail to yield the desired outcomes, we frequently point fingers at the other party, often disregarding our potential contribution to the problem.

This tendency is evident in the way many FSI executives phrase their statements, such as "I did my best, but you know how things are with XYZ in charge at our company. Could you do me a favor?" Meetings are employed to sustain seemingly inconsequential activities while assigning blame to others and creating an illusion of being heard. On one occasion, when I attempted to terminate a series of meetings, an executive candidly admitted they needed a forum to vent. "Yet, no specific actions ever result from it," I responded perplexedly. Nonetheless, they persisted, as the act of complaining was the intended outcome.

Beyond the human aspect, the logical rationale behind this phenomenon is that numerous FSI executives are apprehensive about instigating change. Taking initiative could potentially lead to conflict, jeopardizing their prospects for promotion. Instead, a more calculated approach is to await decisions from higher-ups regarding strategic changes, all the while vocalizing discontent about the present state of affairs.

3. Receiving status updates

Long status updates from management and peers could seem like torture to the average individual. Why not streamline the process by uploading the updates recap to a shared portal and convening only when significant disagreements or intricate questions arise? Many FSI executives relish receiving updates, as they impart a sense of importance and foster optimism that their reports are benefiting from mutual learning. When an employee shares successful strategies, others can organically glean insights, obviating the need for executives to delve into particulars or allocate time to hands-on coaching.

In actuality, these status updates often materialize as a professional circle jerk, where each participant presents their efforts as triumphant. Even someone overseeing a struggling division might frame their updates to sound like success, earning praise from peers, perhaps accompanied by peripheral suggestions. Despite this, the executive at the helm might continue viewing these meetings as valuable learning experiences, as everyone invariably arrives at the subsequent meeting with an apparent positive outlook.

4. Ready to Cancel Meetings - What's Next?

If this newsletter has motivated you to adopt an "anti-meeting" stance as a means to drive digital transformation, where should one begin? By discontinuing and declining participation in recurring meetings, an FSI executive could reclaim an additional 20 hours per week. But how should they best allocate these newfound hours for productive endeavors? It's worth recognizing that digital transformation hinges primarily on personal transformation, and such change necessitates undertaking new tasks using new approaches. This parallels the process of shedding weight and improving physical fitness. In essence, meetings are akin to watching television while indulging in unhealthy food, whereas digital transformation resembles engaging in running paired with intermittent fasting.

Deep thinking about difficult questions

The initial muscle to prioritize is cultivating the skill of deep thinking. While we relish the sound of our voice and recounting "war stories," true transformation underscores the importance of learning over mere explanation. However, when a typical FSI executive claims to have "thought extensively," it often equates to spending perhaps half an hour pondering the thought while perusing LinkedIn or catching up on emails. Consequently, their reflections tend to remain superficial.

As FSI executives evolve into genuine transformational leaders, they encounter an array of intricate questions that necessitate resolution. Taking ownership of these inquiries becomes their duty, eschewing dependence on superiors, peers, subordinates, advisors, or vendors. Addressing each challenging question mandates extensive time—potentially spanning several hours, even dozens of hours—devoted to quiet contemplation, documenting thoughts, conducting research, and multiple iterations.

The VP of Product at Ramp, the fastest growing fintech we previously spotlighted, sheds light on his approach within their deeply entrenched "anti-meeting" culture (listen to the next couple of minutes).

Doing the work

For a typical FSI executive in their 50s, actually doing the tasks seems like a wasted career. They put in those years of menial labor 10-20 years ago, and now they have staff for hands-on execution. Digital transformation requires them to get back into the trenches—not to observe and advise, but to DO — because they don't yet really know what "good" looks like on the next level of digital maturity. How can a leader level up their employees, which is their #1 job, before learning how to do it themselves?

This requirement is not about subjecting an FSI executive to tasks that the most effective executives avoid. Stripe's CTO consistently dedicates time to collaborating with teams on implementing product features. The educational benefit is substantial, and it serves as a profound source of motivation for the teams.

Regular employees dislike meetings, as they are not concerned with shaping perceptions or venting frustrations; their focus lies in creating impactful solutions. Consider the level of appreciation they would show towards an FSI executive who cancels monotonous meetings and, instead, presents well-considered solutions. Even better, if that executive actively participates alongside employees in implementing those solutions.