AI-Native Operating Model Is Taking Shape

Also in this issue: There Is Always a Risk of Incumbents Being Disrupted, but Will It Happen This Century?

AI-Native Operating Model Is Taking Shape

Since Amazon, Netflix, and Spotify's operating models became public by 2012, there was not much new to debate. Sure, more detailed playbooks emerged. Companies moved back and forth on digital maturity and often failed to overcome organizational entropy. But the operating target state was singular. With Block’s Q1-related disclosures, the emerging parameters of the next horizon are now visible for the first time in more than a decade: the AI-native operating model.

In my conversations with FSI and digital-native executives, the most common refrain about Block’s seminal February 26 announcement was “AI washing.” That skepticism is warranted when fintechs like Coinbase cite AI as part of their rationale for cuts even as revenue is collapsing. Block’s context was rather different. The fintech was accelerating growth while already maximizing AI leverage after multiple cuts.

The most unusual part, which made me take the Block announcement in the March 3 newsletter seriously, was the scale of the cuts and where they were made. While 40% was the stated overage, 65% to 75% of eliminated roles appear to have come from the digital core: product managers, designers, and software engineers. Nobody in history has done that, not even Elon Musk at Twitter, and that company was struggling. But there was still a chance Jack Dorsey was pretending to be Elon Musk and making a seemingly insane decision without thinking through the consequences.

Those doubts are starting to subside with Q1 results that only include one month post announcement. The main short-term question was whether such a massive change would damage the franchise’s customer experience and impede growth. Based on March alone, the answer seems to be “no” or at least not yet. Core business growth is accelerating, and the engineering workflow appears to have improved post-change. In a sign of confidence, Block even raised its 2026 performance guidance:

What remains unproven is durability and whether hidden operating risk shows up later in support, fraud, disputes, reliability, and product quality. It will take at least another quarter for Block to prove the following with confidence:

sustained ex-bitcoin growth and gross-profit acceleration across both Cash App and Square

continued meaningful product launches that prove velocity is not backlog burnoff or early AI enthusiasm

a structural product-development OpEx step-down that is not offset by contractors, vendors, AI tooling, management burden, cost shifting, or rising loss expense

no lagged deterioration in release quality, support burden, fraud leakage, disputes, customer/seller complaints, or compliance issues

Another reason for caution is that no other high-performing, large-scale fintech has publicly endorsed Block’s view that the November coding-agent releases were game-changing. In interviews since late February, the leaders of Stripe, Revolut, Nubank, and Affirm either framed the releases as part of ongoing AI-tooling evolution, often focused on expanding output, or outright dismissed the idea of radical operating-model change. For example, Affirm CEO Max Levchin committed to no layoffs, explaining that the fintech is already operating very lean and needs all employees to ship its long backlog of ideas.

For the vast majority of traditional FSIs, this development is mostly academic for now. Even leading businesses within large FSIs are typically years behind Block’s operating-model maturity before its AI transformation. They cannot skip the previous stages of digital transformation and jump straight to an AI-native operating model. For larger FSIs, the most practical question now is whether to pause or keep hiring hundreds or thousands of product managers, designers, and software engineers across the board.

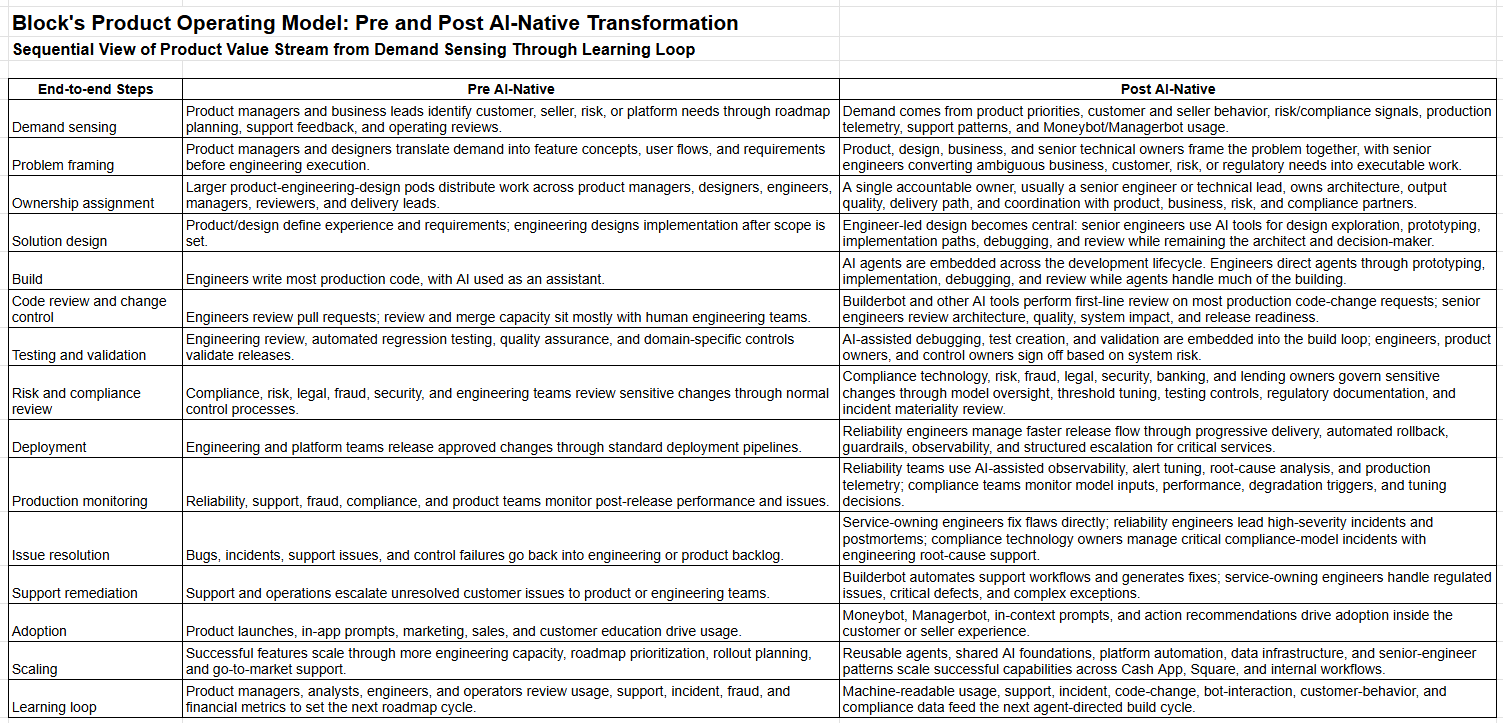

The good news is that if traditional FSIs want to experiment with Block’s operating model in their best cross-functional units, the how is increasingly visible. From Block’s earnings call and open position descriptions, it is possible to compile the new AI-assisted end-to-end process and compare it with the pre-AI-native flow. The difference helps explain how a massive underlying cut in digital roles could be possible. Who will be the first to follow in Block’s footsteps?

There Is Always a Risk of Incumbents Being Disrupted, but Will It Happen This Century?

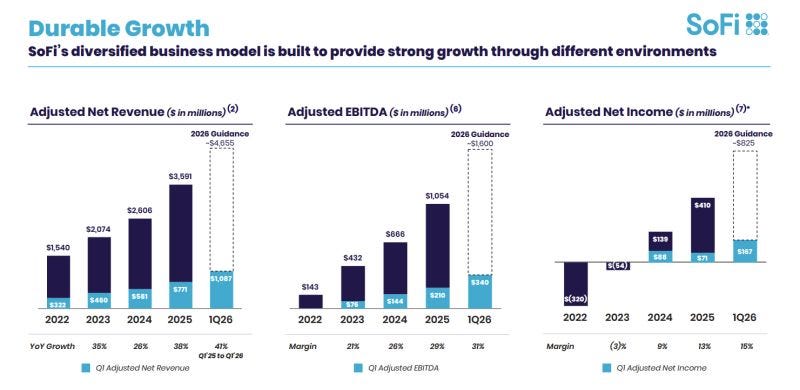

SoFi had a seemingly incredible quarter. It targets upper-middle-class consumers with average FICOs in the mid-700s and offers a broad product set. SoFi also has a bank charter and a revenue-generating technology platform. Yet its stock has halved in six months because those capabilities are not translating into gains in primary banking share or platform sales à la BlackRock’s Aladdin. SoFi still looks mostly like a lending shop chasing every hype cycle in hopes that something sticks.

Chime surpassed 10 million active members, with twice as many new checking account openings as the average incumbent and triple the monthly transactions of a typical fintech. Plus, its newer products generate a third of overall revenue. Chime congratulated itself on leading the market in growth and engagement. Yet none of that proves customer quality or relationship depth, with ARPAM growing only 5% and first-year churn at 50%.

Chime has proved it can scale customers that incumbents do not want across income levels without ripping them off, hence the low ARPAM. The traction with non-struggling consumers in the $75K+ income segment is unknown. This group would make Chime less an auxiliary player serving underserved customers and more a concern for incumbents. Instead, the fintech disclosed similarly low retention and product attach rates.

The prospects of eventual disruption of incumbents are even less hopeful in insurance. Launched in 2016 to disrupt U.S. auto insurance through telematics, Root had all the hallmarks of a software disruptor. Within two years, it was a unicorn. By 2020, it went public at roughly a $7 billion valuation. Then the stock collapsed 99%, staged a violent rebound, and kept swinging, while remaining down 80% from its all-time high. Or, as Root describes the disastrous decade, it consisted of a scale-up, an inflation shock, and a galvanized recovery:

The reality was a self-inflicted strategic mistake. In the wake of George Floyd’s death, most US FSIs and fintechs issued statements and held listening sessions. Root went further, turning credit-score-based insurance pricing into a multi-year marketing and lobbying campaign against incumbent discrimination. The message was powerful: telematics would make underwriting fairer by replacing crude proxies with actual driving behavior.

The problem was that auto insurance is not a morality play. Credit-based insurance scores are controversial, but they are also strong predictors of claims behavior. Auto insurance is already burdened by policy complexity, riders, bundles, regulation, claims uncertainty, fraud, and repair-cost inflation. Trying to grow while relying less on one of the industry’s best risk predictors was underwriting risk dressed up as fairness.

The irony is that Root never fully stopped using credit scores. It promised to eliminate them by 2025, but after the stock collapsed, the strategy shifted, management changed, and capital discipline became existential. The turnaround came only after Root became much more disciplined about pricing, marketing, loss selection, and customer mix. Its CEO later acknowledged that part of the improvement came from attracting preferred, higher-credit customers who behave more responsibly, take better care of cars, and file fewer claims.

To be fair to Root, it is not as if any P&C insurtech has figured out how to compete structurally with incumbents like Progressive. The incumbents have more data, better analytics, stronger balance sheets, and massive distribution advantages. It is not their fault that insurtechs confused risk-based businesses with cute UX wrappers. Disruption prospects are even less likely in life insurance because the product requires motivation from most consumers, which is hard to generate remotely.

Emerging success stories in life insurance also seem to be tackling marginally profitable, underserved segments rather than grabbing desirable customers from incumbents. A meaningful minority of low-intent consumers might be willing to buy online. They were just afraid the process advertised on TV or through referrals would be annoying, opaque, salesy, medically invasive, and delayed. Then Ethos came along.

Multiple attempts by other insurtechs and incumbents to create direct channels in life insurance have either failed or struggled because none have brought together Ethos’ multi-carrier, multi-channel, underwriting-driven distribution platform. Only Ethos combined consumer activation, underwriting, carrier routing, issuance, admin, and ad optimization tightly enough to convert low-intent demand profitably at scale.

For now, life incumbents do not seem to care, since term life is roughly one-fifth of the overall pie. The dynamic is similar to P&C incumbents ignoring Lemonade’s focus on renters and pet insurance. But as Ethos continues to add products and carriers and learns new ways to convert low-intent consumers, the risk exists. Will it follow the path of SoFi, Chime, Root, and Lemonade, or will we finally have a disruptor incumbents actually need to worry about before the end of the century?