Discrimination Across and Within Client Segments, For Lack of a Better Word, is Good for FSIs

Also in this issue: The Failure of the AI-Native Revolution in Financial Services and Insurance; Uber-Like Experience from FSIs: Post-Merger Conversion Edition

Discrimination Across and Within Client Segments, For Lack of a Better Word, is Good for FSIs

Among the general population, there is a myth that some vulnerable customers (by income, gender, ethnicity, etc.) are subsidizing well-off segments. For example, because consumers with high credit scores can get credit cards with lavish rewards, it is implied that low-income consumers are saddled with cards carrying hefty fees and high interest rates.

In reality, FSI products and broader client segments are profitable independently. For example, two-thirds of American Express's revenues come from merchant charges and card fees, rather than from interest on low-income customers (if they have any). A more interesting question is whether to apply digital transformation to amplify different pricing across various identity groups.

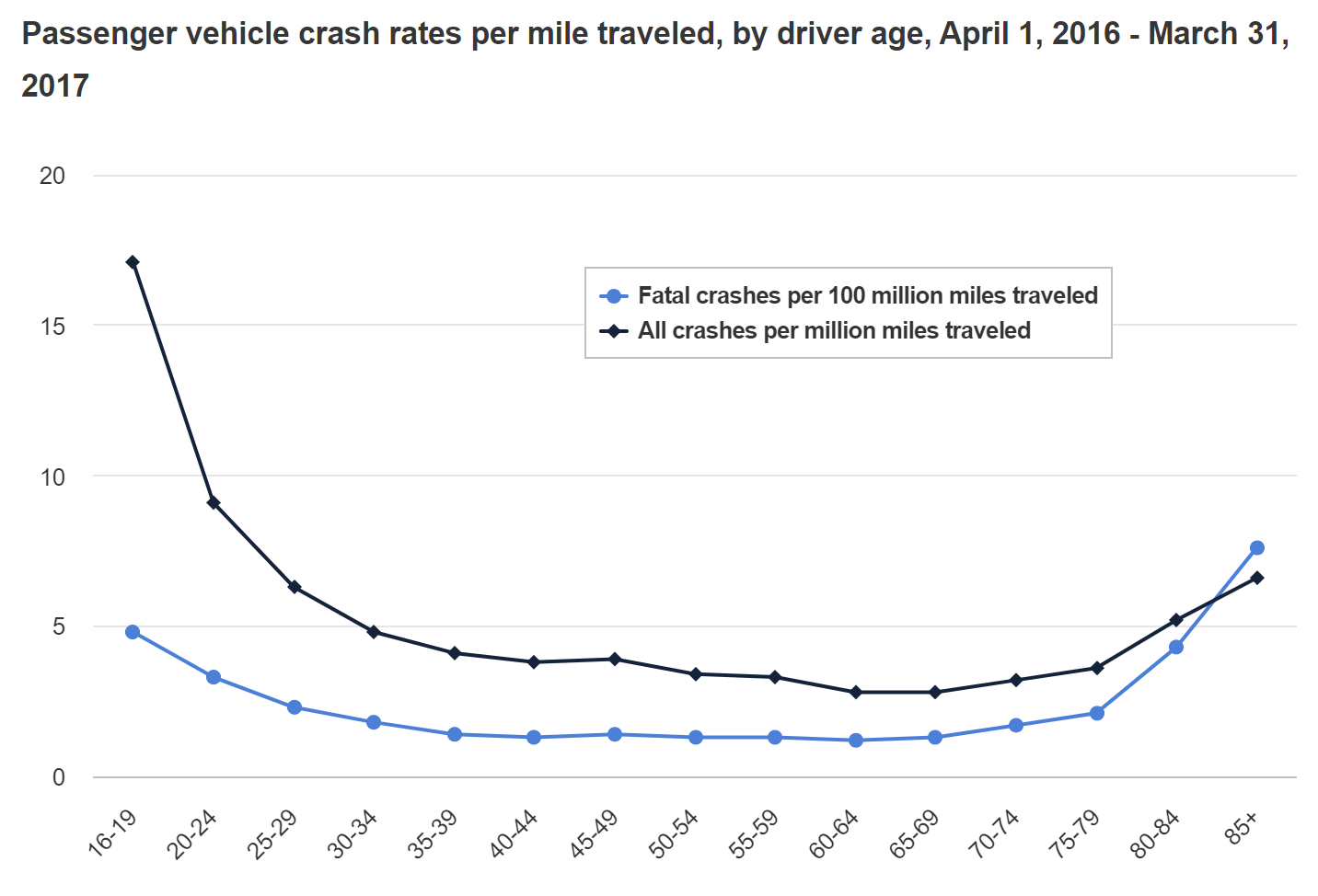

With better data and analytics, FSIs could offer more precise risk-based pricing which could seem like discrimination against the group getting the worse deal. For example, in the US men already pay more for auto insurance than women. What is behind such pricing discrimination?

It is due to men’s generally more aggressive driving behavior. The gap has narrowed somewhat over time, and cars have become safer, but the 2x differential is still there:

With higher digital maturity, auto insurers won’t eliminate the gender gap. Instead, they will widen the in-group differences, with some sub-groups of males getting even higher prices. The obvious factor is a younger age, but some ethnicities are also more likely to drive without wearing a seatbelt or after drinking alcohol.

In the target state of perfect data and analytics, each prospect will be judged only based on their unique risk. However, that wouldn’t eliminate substantial differences in pricing across various identity groups. Besides younger people exhibiting riskier driving behavior, another obvious example is the elderly, 80+ years old:

The hope of digital transformation is in the ever-better matching of a person with their custom financial services and insurance solutions. It should reward better behavior, but it also means that grannies will continue experiencing price discrimination:

The Failure of the AI-Native Revolution in Financial Services and Insurance

Historically, FSI leadership would fight boredom by expanding internationally, conducting mergers and acquisitions, and, of course, re-organizations. But in the last decade, there has been an additional venue for excitement: digital innovations. It started with Agile, then Cloud, and lately, AI.

What is common about these exciting ventures, without an underlying transformation in business and operating models, is their high cost and high degree of failure. Generative AI might seem different since we are constantly hearing about in-production use cases and huge benefits, but no FSI or fintech has yet captured significant efficiency gains.

The latest example of the sleight of hand between revolutionary impact and reality comes from Klarna. Note the future tense of potential benefits and the focus on cost avoidance rather than staff reduction:

“Our AI Assistant will save $40m in CS (customer support) costs, in marketing AI will save $10m… which means we can achieve double digit growth each year without growing headcount.”

Broadly speaking, after almost a decade of so-called AI-native startups, they have failed to revolutionize financial services or insurance, and in some cases, even establish sustainable businesses. Our newsletters often point to firms like Upstart, Lemonade, and Pagaya as illustrations of how AI, by itself, is just a gimmick. “AI Lending Network," "AI Native Insurtech," and "AI-Powered Financing" have become synonymous with disappointing investors, with stocks down 90-95% from their highs.

An even more dire illustration came up recently courtesy of LoanSnap, an AI-based mortgage fintech founded in 2017. Despite raising around $100 million in funding, a recent TechCrunch article uncovered a litany of issues. The fintech missed payroll, got sued by at least seven creditors, went through at least three CFOs, was fined by regulators, was accused of employing unlicensed mortgage brokers, and was pushed for eviction by a landlord:

The charitable explanation is that revolutionizing financial services and insurance takes time. Maybe. The Bolshevik revolution initially wiped out production capacity and caused millions of casualties due to terror and hunger, but three decades later, the Soviet Union became the second global superpower. This is probably not the time frame or impact most FSIs would care for when investing in Generative AI.

In the long term, the AI-native company could become the most intriguing operating and technology model since Smith's division of labor. But for now, nobody, including OpenAI, is ready or has a vision for what it would mean to eat their own dog food. Hence, traditional FSIs would be wise to expect a typical evolution like with any novel technology rather than worrying about missing an AI revolution.

Uber-Like Experience from FSIs: Post-Merger Conversion Edition

FSI executives like to repeat in interviews that their customers demand the same experiences from financial services and insurance as they get from their favorite apps like Uber. While catchy sounding, this also sets those executives up for certain failure since FSI products are much more complex. Even the apps of the best fintechs start looking clunky as they add more products and features. A different level of complexity also amplifies fundamental differences in customer preferences for UX journeys - satisfying one segment's preference comes at the cost of another.

Such a disconnect between unrealistic expectations and otherwise reasonable service quality came to a head during the recent post-merger cutover of First Republic Bank (FRB) customers into JPMorgan Chase, which created a barrage of online complaints. Post-merger go-lives have been known for horror stories over the decades, so how badly has JPMC screwed up? It did not. The work was completed over the Memorial Day weekend:

“By Tuesday morning—the first business day—all of our systems were fully operational,” the spokesperson said. “In fact, it was our smoothest major migration ever.”

When BMO bought Bank of the West, it had a similar conversion, except over the Labor Day weekend last year, with everything working smoothly afterward.

What JPMC leadership did not anticipate was that the FRB client base included a lot of executives from high-tech and VC industries, plus demanding business owners. These types not only tend to work on weekends but also think that their FSI should give them an Uber-like experience. A recent Wall Street Journal article offered multiple examples of those clients' disappointment:

“…the embarrassment of having your card declined for transactions, despite assurances that everything would work smoothly.”

“…hasn’t been able to access about $50,000 he kept in a small-business account at First Republic… customer-service representatives couldn’t locate his account.”

“…spent over six hours each day on Memorial Day weekend trying to access his accounts and set up autopay on some construction loans.”

When working with FRB many years ago, I was struck by how little value they placed on technology. Their phenomenal growth, which regulators were even trying to slow down at some point, was based on the high-touch engagement by their relationship managers. JPMC didn’t have to have a seamless conversion or make that experience as easy as updating an Uber app - instead, it should have reached out to each client personally, ideally with a phone call, to set expectations for some temporary dysfunction over the weekend.